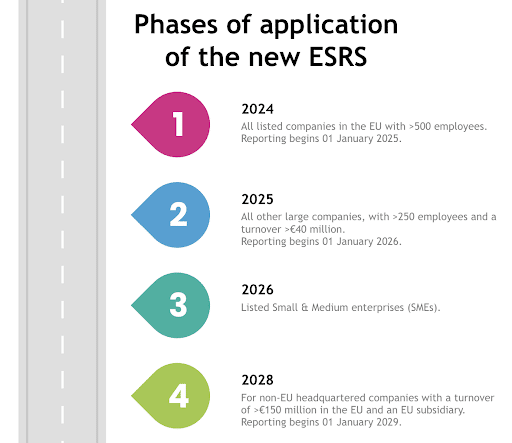

In November 2022, the European Parliament overwhelmingly approved the new Corporate Sustainability Reporting Directive (CSRD), creating the new European Sustainability Reporting Standards (ESRS). The first set of ESRS were approved by the European Financial Reporting Advisory Group (ERFAG) board on November 15, 2022, and is expected to be adopted by the European Commission by June 2023 (1). It will apply to an estimated 50,000 large and listed European Union (EU) companies and, in the future, to all third-country companies. These ambitious standards aim to foster greater transparency and accountability and push for transforming companies’ ESG ambitions. It will be implemented in four different phases (2).

Given the speed of application of the ESRS, companies need to act fast and assess their readiness to comply with these new rules and their potential impact. While global companies headquartered outside the EU have more time, they need to start planning for 2028, when they will need to report data on the upstream and downstream of their value chains (3).

What is in the European Sustainability Reporting Standards?

Currently, only 10 ESRS have been finalised, with more on the way. There is, however, a common structure across ESRS. Companies will need to report on the following:

| Reporting Areas |

Topics |

Reporting Layers |

|

|

|

|

|

|

|

|

- Impact, risk, opportunity management and metrics

|

|

|

|

|

|

|

These three layers are intended to provide a flexible framework allowing companies to report on the issues most relevant to their operations and stakeholders. The CSRD and the ESRS require companies to consider “double materiality” when submitting their reporting, meaning that they must consider both the materiality of sustainability issues to the company and the materiality of those issues to their stakeholders. Companies must also submit prospective information about their upstream and downstream value chains.

European Sustainability Reporting Standards push for transformation

Adapting to these new standards will require a significant investment in resources and technology. Companies will need to invest in systems and processes to track and measure their ESG performance throughout their value chain, as well as the necessary training and support for employees to understand and implement these changes (4). Given the double materiality and the link created by ESRS between financial performance and environmental and social impact, companies will need to analyse gaps in their data gathering and revisit their operations and value chains to identify areas of improvement and transformation to improve their ESG performance (5).

Overall, the adoption of these new European Reporting Sustainability Standards will present both challenges and opportunities for companies as it will increase the attention of consumers and investors on ESG metrics. While it will require a significant shift in business strategies and a commitment to sustainability, it will allow greater transparency and allow companies to gather the insights they need to transform their operating models. As countries across the globe are becoming increasingly aware of the need to become more climate ambitious, many will probably take inspiration from EU legislation.

Summary and key takeaways

- Sustainability performance will be at the top of companies’ agendas, alongside business strategy and annual financial performance.

- The European Sustainability Reporting Standards (ESRS) will apply to an estimated 50,000 large and listed European Union (EU) companies and eventually apply to third-country companies with operations in the EU.

- Access to quality data and data analytics are major challenges in fulfilling the ESRS requirements.

- Adapting to the ESRS will require a significant investment in resources and technology, as well as training and support for employees to understand and implement the changes.

- The adoption of the ESRS presents challenges and opportunities for companies, as it will increase attention on ESG metrics and link them to financial performance. It will require a commitment to sustainability and allow for greater transparency and the opportunity to transform operating models.

Want to learn how we can help you assess your ESRS readiness and help embed your ESG strategies in your business operations? Reach out to our team here.